NVDA and the New Cold War Economy

Export bans, inventory hits, and the slow grind of tech decoupling.

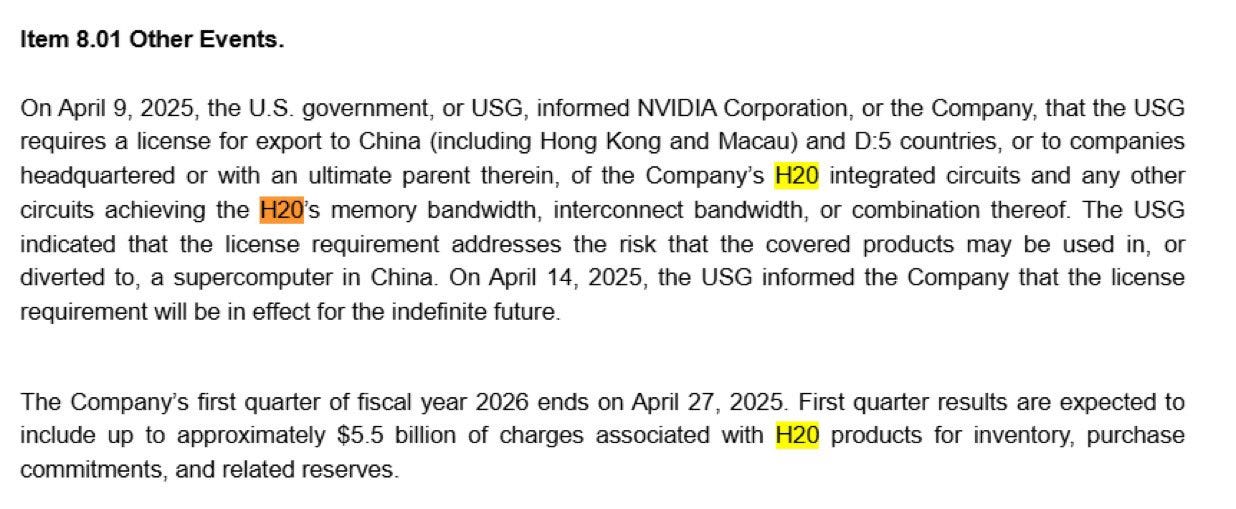

After regular trading hours today, NVIDIA disclosed that its H20 chip—designed specifically to dodge prior U.S. export restrictions—has now been swept into new licensing requirements from the U.S. government. This isn’t about tariffs. It’s not about trade fairness. It’s a direct enforcement move against contravention of U.S. national security policy. And it came with a hammer: NVDA expects up to $5.5 billion in charges this quarter linked to H20 inventory and purchase commitments.

The market reacted fast. NVIDIA dropped 7% in aftermarket trading. Given its oversized weight in the S&P 500, that dragged index futures down 70bps on the Asia reopen. This wasn’t just a chip headline—it was a macro event.

We’ve said it before: 2025’s drawdown has felt vibes-driven, not data-driven. But we warned that the data would come. This is it. NVDA is the first big provisions-led tape bomb of this cycle. It won’t be the last.

Second-Order Effects

(1) The Whole AI Supply Chain Is in the Blast Radius

If H20 is no longer safe, what about other “compliant” SKUs? Look for potential collateral damage across AMD, Broadcom (custom silicon exposure), and TSMC (contract fab risk). Even ASML could wobble if enforcement extends into equipment supply.

(2) China Demand Risk Repricing

This isn’t just about chips. U.S. policy is now aiming to kill demand inside China, not just restrict what gets sent there. Cloud and hyperscale buildouts from firms like Alibaba, Baidu, Tencent—all dependent on H20—could slow dramatically. That puts Chinese tech ETFs and the Hang Seng Tech Index at risk of further derating.

(3) Inventory Risk Across the Board

NVDA just guided for $5.5B in related charges. Who else is sitting on suddenly-useless inventory built for restricted geographies? Watch for earnings bombs from OEMs, board-makers, and hyperscalers exposed to China-based capex plans.

Third-Order Effects

S&P 500 Concentration Cuts Both Ways

NVDA’s fall illustrates the risk of an index so top-heavy. If tape bombs keep hitting the megacaps, passive flows will amplify downside. Expect volatility in QQQ and SPX even if rate or inflation narratives remain benign.

Washington Will Keep Moving the Goalposts

H20 was supposed to be safe. It’s not. Expect markets to reassess the durability of all workarounds—whether in chips, EVs, batteries, or renewables. This undermines confidence in any corporate guidance tied to policy interpretation. It’s a new regulatory risk regime.

The Mood Has Shifted

We’ve gone from speculative rally to earnings downgrades. Investors who were happy to buy dips on vibes now have to reckon with tangible hits to earnings and cash flow. Risk premia are adjusting accordingly.

Bottom Line

This isn’t an isolated event. NVDA just taught us what the next leg of this market looks like: tape bombs, inventory write-downs, geopolitical enforcement, and a grinding revaluation process. We remain in a bear market. And now, the data is finally catching up to the mood.

Stay sharp, trade your edge.